Effective January 1, 2018, the Tax Cuts and Jobs Act (“TCJA”) made temporary changes to the Estate, Gift and Generation Skipping Transfer Taxes (collectively, “Transfer Taxes”) which could dramatically affect how our clients plan for the future and the outcomes of their estate plans.

Exemptions and Planning. Prior to enactment of the TCJA, the first $5 million (as adjusted for inflation in years after 2011) of transferred property was exempt from Estate and Gift tax. For estates of decedents dying and gifts made in 2018, this exemption as adjusted for inflation would have been $5.6 million per person, or $11.2 million for a married couple (“Transfer Tax Exemptions”).

Many estate plans anticipated that Transfer Tax Exemptions would remain at a certain level. As such, our clients often rely on the Exemption amounts to determine how much a charitable organization, surviving spouse or children would receive as their inheritance.

Transfer Tax Exemptions Doubled. The new law temporarily doubles the amount that can be excluded from these Transfer Taxes. For decedents dying and gifts made from 2018 through 2025, the TCJA doubles the base Transfer Tax Exemptions from $5 million per person to $10 million per person. Indexing for post-2011 inflation, brings this amount to approximately $11.2 million per person for 2018, and $22.4 million per married couple. The Exemptions having doubled in size will result in many fewer estates being subject to the 40% tax, in addition to larger estates owing less tax overall.

A related Transfer Tax called the generation-skipping transfer (“GST”) tax is designed to prevent avoidance of estate and gift taxes by skipping transfers to the next generation. The TCJA does not specifically mention generation-skipping transfers, but since the GST Exemption amount is based on the Transfer Tax Exemptions, generation-skipping transfers will also benefit from the post-2017 increases. Thus, the TCJA could also double the amount going to the GST exempt portion of an estate plan, and eliminate the amount going to the GST-non-exempt portion of an estate plan.

Effect on Estate Plans and Gifting. The increased Transfer Tax Exemptions have the potential to greatly impact your current estate plan and cause you to consider the need to redraft some important documents. For clients who referenced Transfer Tax Exemptions as part of their planning, the TCJA may effectively double the amounts going to Estate Tax-exempt portion of the estate plan and eliminate the amount going to the Non-Exempt portion of the estate plan. As a direct result of the TCJA, this could mean that the amount going to a charity, spouse or children, if tied to Transfer Tax Exemptions, had two very extreme changes: it could be that the exempt portion going to children doubled; it could also mean that the non-exempt portion going to a charity or spouse is entirely eliminated; finally, it could mean the opposite or anything in between.

Further, the unused portion of a deceased spouse’s estate tax exemption may still be added to that of the surviving spouse using a tax election known as “portability”.

Another potential affect will be a shift from Transfer Tax planning to income tax planning. For example, from an income tax planning perspective, the use of a limited liability company (LLC), family limited partnership (FLP) or an Irrevocable Trust may no longer be necessary.

In the past, under a more traditional planning model, our clients have considered avoiding Transfer Tax by gifting low basis assets to their families. By gifting, our clients avoided a 40%-55% Transfer Tax rate in exchange for a 20% capital gains tax rate. Therefore, now that the imposition of Transfer Tax has been eliminated for 99% of all individuals, everyone should reconsider the tax and economic value of gifting low basis assets to their children.

Further, prior to considering any case studies, we suggest reviewing a recent history of the Transfer Tax Exemptions.

How to Address “Temporary” Changes. The changes contemplated by the TCJA are set to expire within eight years. In a vacuum, it can be extremely difficult to anticipate what will occur when the TCJA expires. As such, many academics and professionals are hesitant to recommend treating these changes as permanent. Their caution is that the Trump administration will not last past 2025, and that a Democrat successor to President Trump will allow these changes to expire by simply doing nothing.

Under this line of thinking, there is no guarantee that the Congress and President elected in 2024 would allow the changes in TCJA to expire. The TCJA has similarities to recent legislative history. In 2001 President Bush increased the estate tax exemption over a period of ten years from $675,000 to $3.5 Million. In 2010, the estate tax was entirely repealed for one year, and in 2011, the changes were set to revert to what was in place in 2000. However, in December of 2010 President Obama signed legislation which again increased the Transfer Tax Exemptions (including Gift and GST Exemptions) to $5 million for a temporary period of two years. Then in 2012, the changes enacted in 2010 were made permanent through additional legislation signed by President Obama.

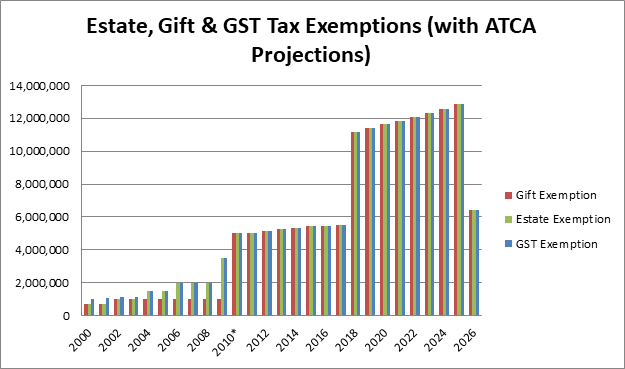

We believe it is important to address the history of the Transfer Tax Exemptions in order to more appropriately project what will happen after the provisions of the TCJA expire. To that end, below is a graph of the historical Transfer Tax Exemptions, with the projections for the next eight years.

*In 2010, the Estate Tax was repealed, but there was an option to elect into the Estate Tax Regime.

The trend over the past forty years has been to increase the Transfer Tax Exemptions. While the above chart illustrates dramatic increases over the last two decades, large increases have occurred since 1981, when the estate tax exemption was $175,000.00. As a result, Transfer Tax collections as a percentage of federal revenues have decreased. For the past several years, Transfer Taxes have made up less than 1% of federal revenues. For example, see https://taxfoundation.org/estate-tax-provides-less-one-percent-federal-revenue/.

It is certainly possible that a successor administration will allow the TJCA increases to expire or will enact more limiting legislation of their own. However, the history of the Transfer Tax Exemptions and current trends may not support that possibility. Inasmuch as the amount of federal revenue associated with Transfer Taxes is minimal, and the costs associated with compliance are high, the upward trend in Transfer Tax Exemptions could very well continue into 2026 and beyond. There is good reason to integrate these changes into your plan.

In any case, the underlying assumptions used to create estate planning documents just a few years ago have dramatically changed. For most, the possibility of a Transfer Tax problem has been eliminated. For those who may still have taxable estates, the amounts which are paid to various persons under the plan may change profoundly, if inheritance amounts are tied to the increased Transfer Tax Exemptions.

If these assumptions remain unchanged, the administration of estate plans for persons who made no update to their plan may result in drastically different tax and economic outcomes. As a result, all should consider the impact of the law on their particular situation. If you would like to schedule a brief review, please give us a call.